Oil Price Fluctuations and the Power of OPEC

A wild recent day for oil prices demonstrates OPEC’s enduring influence.

Last week Saudi Arabia announced that it will reach $300+ billion in government revenues for 2022. Oil prices were increasing even before Russia invaded Ukraine, and it has been a very profitable year for Saudi Aramco and other oil producers around the world.

Part of the story is OPEC’s continued ability to exercise market power. For today’s post, I want to look at a recent day in oil prices that provides a striking example.

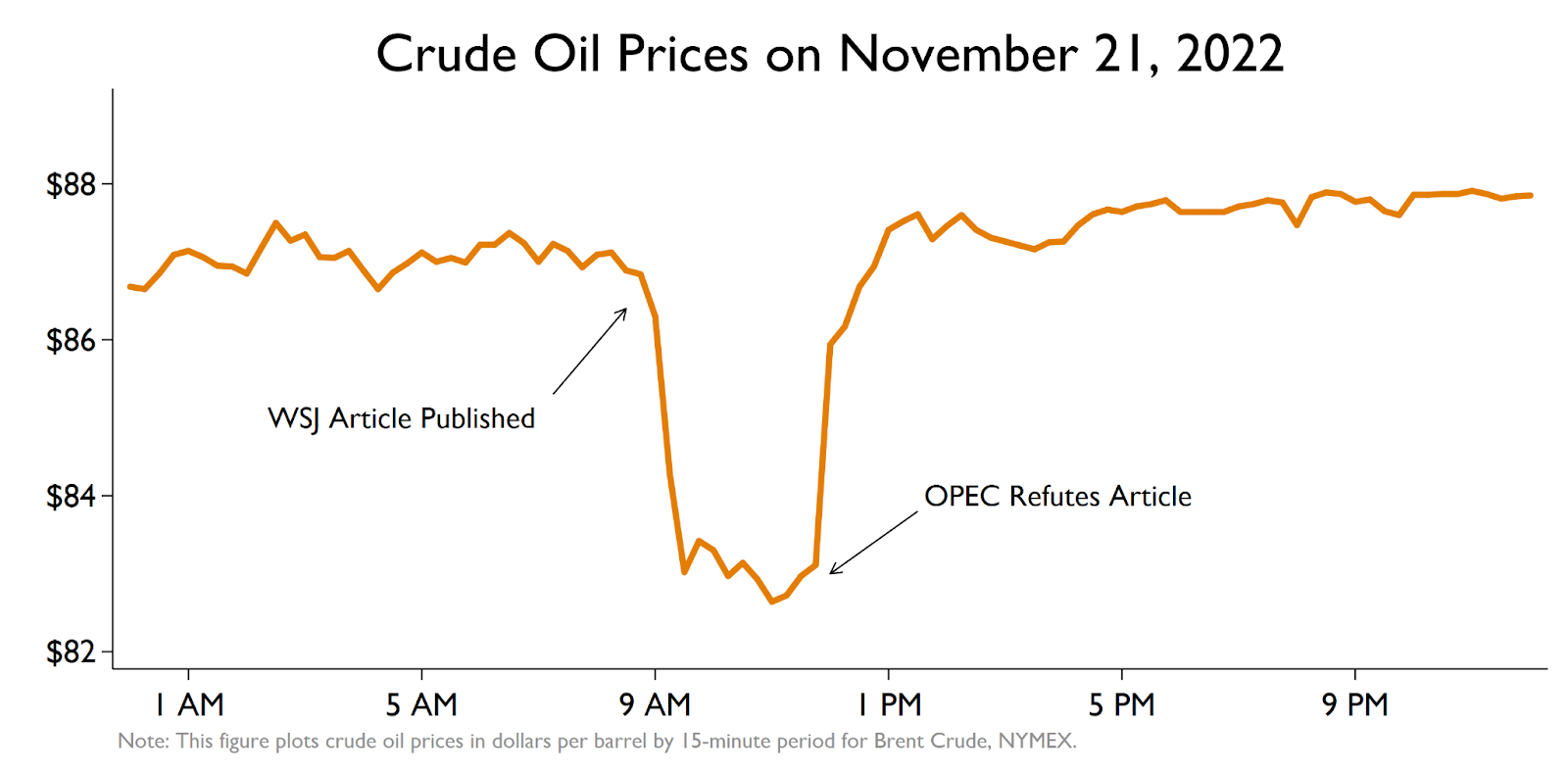

November 21st started out like a normal day, with crude oil trading steadily at $87 per barrel. Then, all of a sudden, prices plunged $4 per barrel, only to, hours later, rocket right back up to where they started.

This rapid plunge and rebound illustrate the enduring power of OPEC to influence oil prices. It shows how even small changes in expectations about OPEC behavior can have big effects on the global crude oil market.

Boomerang

It all started at 9am Eastern when the Wall Street Journal published an article about OPEC on its website. The article reported that OPEC was considering a 500,000 barrel-per-day increase in production.

This was big news because it would have marked a distinct change in strategy for OPEC. And oil prices plummeted immediately from $87 to $83.

–

Hours later, Saudi Arabia’s energy minister put out a statement strongly denying the article. The statement emphasized that not only was OPEC not discussing an increase, but that they stand ready to *reduce* production if needed to balance supply and demand.

And, just like that, prices rocketed back up. In the end, oil prices ended up right back where they started. The figure above plots prices for Brent crude. Axios’ Matt Phillips has an excellent related piece including a figure showing an almost identical pattern for WTI crude.

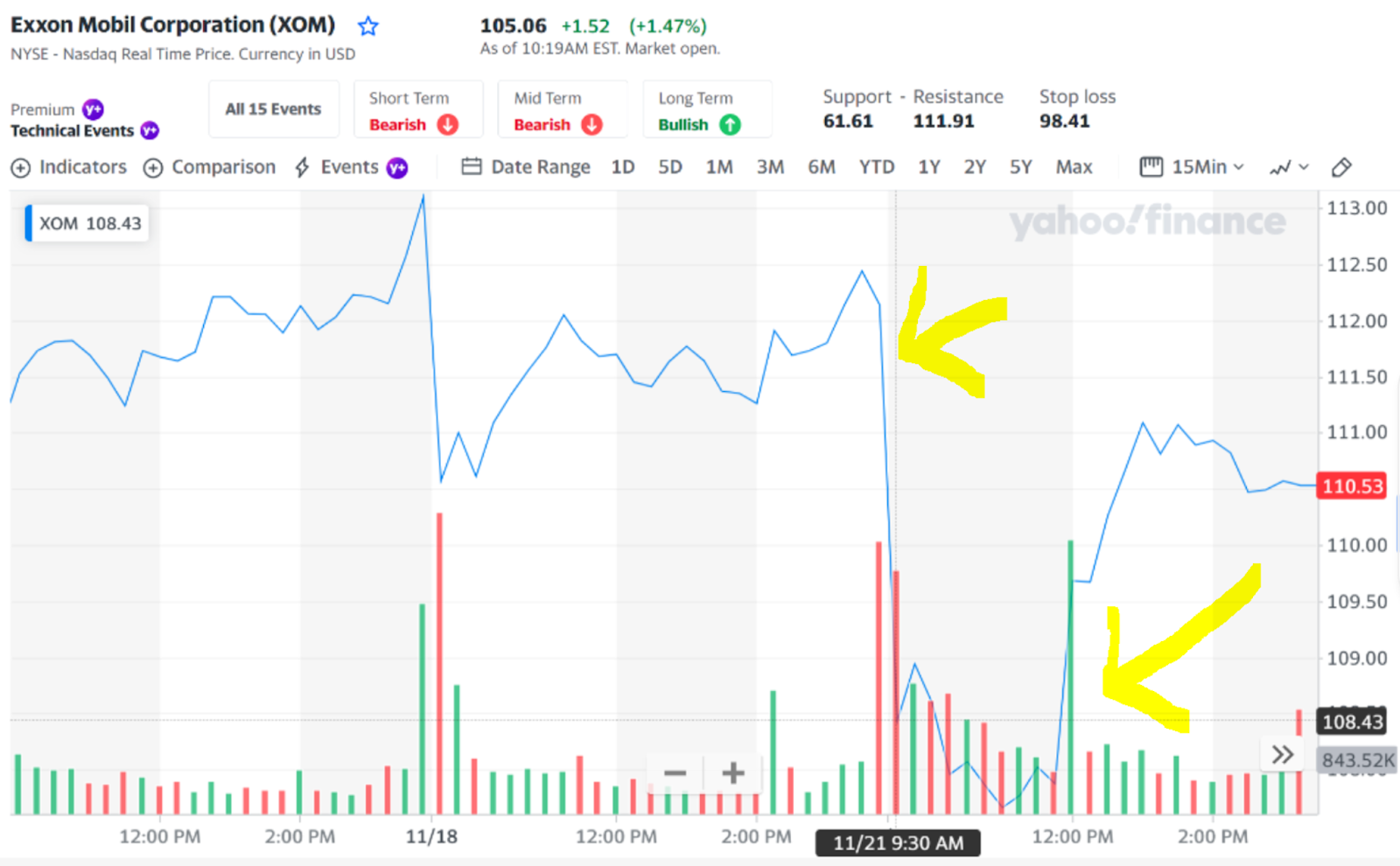

This is a significant price movement. Global oil production is 100 million barrels per day, so $4 translates to $400 million per day, or $12 billion per month. Moreover, oil company valuations respond to these changes. Exxon Mobil’s stock price, for example, fell at 9am from $112 to $108, and then rebounded around noon back to $111.

–

Deja Vu

This large price swing is all the more remarkable because at issue is a relatively small change in supply. An increase of 500,000 barrels is only half of 1% of global oil production.

But when it comes to the oil market, even small changes in supply or demand have big effects on prices. We saw this in 2008, 2014, and again, most recently, in 2020, when crude oil prices plummeted in response to what was initially a relatively modest decline in global oil demand.

Why are oil prices so sensitive? Because both supply and demand are highly inelastic.

On the supply side, there is limited flexibility for other producers to change output over a short time horizon. Research by Energy Institute alum Ryan Kellogg and coauthors has shown that U.S. oil production from existing wells does not respond to oil prices. Yes, producers drill more wells when prices go up, but it takes months for this to result in higher production.

And the story is similar on the demand side. Over a short time horizon, there is little that you or I can do to change how much oil, gasoline, or diesel we use. Sure, we can keep our tires properly inflated, and take other modest actions, but over a short time horizon the overall price elasticity of demand for oil is low.

–

Dominant Producer

Last week OPEC met again and, even though the meeting was held virtually, there were still dozens of journalists crowding around the OPEC office in Vienna, hoping for some kernel of news. Any information about OPEC’s plans is so valuable, that it makes sense that these meetings are closely followed.

Was OPEC really discussing a production increase in November? Who knows? The WSJ attributed this information to conversations with “OPEC delegates”, and other media sources made similar reports.

Regardless, the episode is a compelling illustration of OPEC’s ability to influence prices. In this market, all it takes is a short conversation with a journalist, or a press release from the Saudi energy minister, to have a big impact on prices and profits.

–

Keep up with Energy Institute blogs, research, and events on Twitter @energyathaas.

Suggested citation: Davis, Lucas. “Oil Price Fluctuations and the Power of OPEC,” Energy Institute Blog, UC Berkeley, December 12, 2022, https://energyathaas.wordpress.com/2022/12/12/oil-price-fluctuations-and-the-power-of-opec/

Categories

Lucas Davis View All

Lucas Davis is the Jeffrey A. Jacobs Distinguished Professor in Business and Technology at the Haas School of Business at the University of California, Berkeley. He is a Faculty Affiliate at the Energy Institute at Haas, a coeditor at the American Economic Journal: Economic Policy, and a Research Associate at the National Bureau of Economic Research. He received a BA from Amherst College and a PhD in Economics from the University of Wisconsin. His research focuses on energy and environmental markets, and in particular, on electricity and natural gas regulation, pricing in competitive and non-competitive markets, and the economic and business impacts of environmental policy.

Very believable. Years ago, my student, Ali Johanny, wrote thesis and then book claiming that dominant-firm price leadership was the right model and that Saudi Arabia was the leader. I found it convincing.

If OPEC has such great market power one might wonder how the price of Dated Brent (the price published by Platts which is used for many of the physical transactions in oil, not the NYMEX Brent futures contract cited here which today had exactly 0 transactions and 0 contracts open) fell from $101.71 on November 7 to $76.35 on December 8?

The fact is all commodity markets are subject to large swings. I have explained this to students, noted it when doing my Ph D at MIT and written on the subject extensively. Jeff Williams, a professor at USC Davis described the behavior in his book “Manipulation on Trial” which focused on the fluctuations in silver prices in the early 1980s.

If you want to find a real price swing look back to January 17, 1990. On that day Brent was quoted at $30.17/bbl. On the following day Platts put the price at $19.25/bbl. What explains the drop. As the “Washington Post” wrote “Traders and industry analysts attributed the sharp drops to euphoria over the seeming success of the attack on Iraq and the release of 2.5 million barrels of oil from strategic reserves in the United States, Japan and Europe — a move that increases already plentiful world supplies of oil and puts further downward pressure on prices.”

The post by Professor Davis is off the mark.

The implicit model behind this story seems to envision an OPEC monopoly with a competitive fringe wherein the monopolist can quickly make substantial changes in production but the competitive fringe can’t. But why don’t the Ryan et al. “Hotelling under Pressure” limitations apply to OPEC?

A more complete model might also account for inventories. The rumor about increased OPEC production signals that inventories are too large, i.e. demand in the very short run shifts down. Or are inventories inflexible too?

This short run fluctuation can be used for a back-of-the-envelope estimate of the sum of supply and demand elasticities (both in absolute value). Short run expectations were for a 0.5% exogenous increase in supply. The price response was a quick drop of 4.6%. The sum of elasticities needed for this price change to soak up this sudden excess supply is equal to the percentage change in supply divided by the resulting percentage change in price. This ratio equals 0.11, an estimate of the sum of these two elasticities.

This accords with other sudden shocks to oil supply and prices in other periods. I’ve used this as the basis of simple problem set questions in my energy economics class. Looks like you have a cool new problem set question.

Interestingly, you can do the same kind of back-of-the-envelope calculation for other commodities, and at least for all the ones I’ve looked at, you get something similar: in the ballpark of 0.1 for the sum of supply and demand elasticities. It’s also the approximate number we found for global agricultural commodities using a somewhat more complicated approach.

A classic oligopolist set of actions and your graphs point out very short term effects. So should you reduce their power and if so, how do you reduce their power?

Develop a country that controls its own energy infrastructure for itself and its allies, which also reduces our strategic and military interests in protecting the middle east’s oilfield. Yergin was right a long time ago, and its time we committed to flipping the script.

Develop and nurture ALL their competitors, whether its short term, (he didn’t just say) domestic oil and gas production, or long term, EV transportation, or really long term, fusion. Export that energy as President Obama allowed after a 40 year ban. Now we can possess the strategic power and set an example for the rest of the free world.

Oil & gas are highly fungible goods where prices in other global locations set U.S. prices as well. (Name me another commodity where the U.S. price is set at location in another country, e.g., Brent?) This makes chasing “energy independence” through increases oil & gas production, e.g., developing the North Slope, a waste of time. It only enriches the large multinational oil companies that have no allegiance to the U.S. The only viable alternative is developing non-petroleum resources for which pricing can be relatively isolated, such as renewables.