39% Plugin Vehicle Share In China! — China EV Sales Report

Plugin vehicles are all the rage in the Chinese auto market. Plugins scored over 750,000 sales last month, up 36% year over year (YoY) and a new record. That pulled the year-to-date (YTD) tally to over 4.6 million units.

Share-wise, with August showing another great performance, plugin vehicles hit 39% market share! Full electrics (BEVs) alone accounted for 26% of the country’s auto sales. This kept the 2023 share at 36% (24% BEVs), and considering the current growth rate, we can assume that China’s plugin vehicle market share will end over 40% by the end of 2023.

Another measure of the importance of this market is the fact that China alone represented close to 60% of global plugin registrations last month!

Looking at August’s best sellers in the overall market, we see plugins populating the top positions, with 4 plugin models in the overall top 5! The best selling ICE model showed up only in 5th! And to think: in other markets, we celebrate when one EV breaks into the overall top 10….

Breaking down sales by vehicle size, the picture hasn’t changed much in the past few months. The A (city cars), B (subcompacts), and D (midsize) segments are heavily electrified, while the C (compact) and E (full size) segments still have a strong ICE presence.

In the E segment, “premium-ness” still has a strong effect and the German Three Maries (Audi, Mercedes, and BMW) have an important presence. (It is no coincidence that, among European OEMs, they are the ones less interested in a tariff dispute with China — it could wipe them out of the profitable Chinese market, something other European OEMs are less exposed to.) It is more intriguing why the compact category is still so ICE based. Coincidentally or not, it is the only segment where BYD does not have a clear sales champion — the Yuan Plus crossover is more focused on export markets; while the e2 hatchback is, well … a hatchback, so that alone already limits its sales potential in this category; and the Dolphin, despite size wise sitting somewhere between the B and C segment, in reality is playing in the smaller category.

So, there is an opportunity for BYD to provide a new model and cover this C-sized hole. And with the current wave of new BYD models filling every niche, real or imaginary, it is intriguing that it hasn’t realized this. Or maybe a new BYD e3 (a sedan version of the e2 hatch) is coming along soon?… Or maybe even a Baby Seal?

The 20 Best Selling Electric Vehicles in China — August 2023

Here’s more info and commentary on August’s top selling electric models, again with only BYDs and Teslas in the top 5:

#1 — BYD Song (BEV+PHEV)

BYD’s midsize SUV was again top dog in the overall Chinese automotive market, with BYD’s current star player scoring 56,743 registrations, 9,043 of them belonging to the BEV version, which is a new record. Will the Song end the year as the best selling model in the Chinese automotive market? At this point, it is likely. Looking at the internal competition, the Frigate 07 PHEV has failed to make a dent in its sales, while its premium cousin, the Denza N7, also doesn’t seem able to divert a sizable level of demand away from it — if nothing else, because it lacks a PHEV version. The real internal competition could come in the form of the upcoming Song L, BYD’s take on the Model Y theme, but that should only impact sales next year, not this one. With the Song’s current trend of selling 50,000+ sales/month, there is no major reason why it won’t continue leading the cutthroat Chinese auto market this year.

#2 — Tesla Model Y

Tesla’s star model got 51,117 registrations, so it seems the price cuts continue to spur demand for the US crossover. At a time when Chinese automakers are in peak form, Tesla is currently the only foreign OEM able to follow the amazing pace of domestic carmakers. The Model Y’s most immediate threat is actually coming from its own stable in the form of the refreshed Tesla Model 3. While the refresh on the sedan wasn’t as deep or disruptive as some expected (more on this in the Europe article), the new interior and updated specs could allow the sedan to start cannibalizing some volume from its crossover sibling during the coming months…. Watch this space in Q4.

#3 — BYD Qin Plus (BEV+PHEV)

Thanks to a refresh and price cut, the BYD Qin Plus has been rejuvenated and its sales have jumped back again. The midsizer reached 42,808 registrations in August, with the BEV version alone scoring 11,654 registrations. With prices now starting at 100,000 CNY ($15,000), demand is again strong, despite the fierce internal competition (the BYD Seal for the BEV version and the Destroyer 05 for the PHEV version). Expect BYD’s lower priced midsize sedan to continue posting strong results, at the cost of its most expensive siblings. It should have no problem keeping its most direct competitors at a safe distance, with the likely exception of the refreshed Tesla Model 3 Performance in December, which should be amazing, but not enough to remove the Qin Plus from the leadership in the midsize sedan category in the whole year of 2023.

#4 — BYD Seagull

With 34,841 registrations, in only its fourth full month on the market, BYD’s future star player is ramping up fast. The question now is: How high will it go? In its domestic market of China, it could win a best seller title by the end of the year (November?) but it is overseas that the little EV could be a true disruptive force: Latin America and Africa are waiting for a good, cheap EV that can push EVs into the mainstream, and the Seagull could be it. And this could be the model that places BYD among the best sellers in places like India and Europe — where good, small, value-for-money BEVs are scarce. Sitting somewhere between the A and B segments, at 3.78 mt, and using a purposeful angular design, it profits from the brand’s leading Blade batteries, in 30 kWh and 39 kWh sizes. It starts at 74,000 CNY (+\-$10,500 USD). The only model rivaling it is the slightly larger (3.95 mt) Wuling Bingo, which starts at 60,000 CNY (+\-$8,200 USD), but at that price, it comes with a battery of just 17 kWh and no DC charging. For a similar-spec Bingo, equipped with a 32 kWh battery & DC charging, it starts at 74,000 CNY, the same price as the Seagull. So, spec-wise, both seem equally competitive, but the Seagull benefits from the current strength of the BYD brand, something that the Wuling EV lacks. Also, does SAIC (or GM) have export plans for this small EV?

#5 — BYD Dolphin

The small-to-compact Dolphin scored 31,096 registrations, a near-record for the space-efficient EV. With the small EV now starting to send units to export markets, it seems that BYD is happy to have it running at around 30,000 units/month in its domestic market. This should still allow him regular presences in the Chinese top 5. Expect the Dolphin to become BYD’s second Musketeer in overseas markets, joining the current Yuan Plus/Atto 3 crossover and the upcoming Seal sedan, which will stand as a solid honor guard to the future D’Artagnan of the lineup, the BYD Seagull.

Looking at the rest of the table, the main highlight in the top half is the #6 GAC Aion Y scoring 26,713 sales, a new record performance. It not only beat the category leader BYD Yuan Plus, but is also now looking to break the glass ceiling disrupt the BYD/Tesla duopoly at the top! Will the MPV-disguised-as-a-crossover get there?

Further below in the table, a highlight was in #14, with the BYD Destroyer 05 scoring a record 12,092 registrations. It proves that even the bench players in the BYD lineup are able to present great results. Elsewhere, Li Auto placed all three of its models in the top 20, with the L9 seven-seater — the startup’s biggest model — having another record month (10,933 registrations). Imagine that, a Cadillac Escalade–like plugin selling over 10,000 units per month….

Note that the L9, L8, and L7 are all full-size SUVs. Last month, there were four models larger than 5 meters in the top 20 — the Li Xiang L9, L8, & L7 as well as the Denza D9. Talk about automotive obesity….

The hot startup brand has a winner trio on its hands. The cheapest model in the startup’s lineup (starting at $49,000) should continue to improve its standing in the near future, with Li Auto setting a bullish sales target of 400,000 units this year! And 800,000 in 2024!! And 1.6 million in 2025!!! :0

For these targets to be met, the midsize L6, due to be launched sometime next year, will be a critical part of the puzzle.

Still on the topic of the top 20, the other big news is Leap Motor’s C11 midsize SUV joining the table, in #19, with a record 10,209 units. That’s mostly thanks to the BEV version, which amassed a record 6,602 registrations, thus providing much needed volume to the startup.

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Outside the table, the highlights are varied. In the fresh blood startup category, XPeng’s take on the Model Y theme G6 midsize SUV got 7,068 registrations, in only its second month on the market. The new model should join the top 20 soon, as ramp-up continues. The struggling startup threw everything but the kitchen sink at its new model, so that it finally has a winner on its hands.

In a slightly better position, we find NIO, with the new generation ES6 midsize SUV selling quite well (8,601 units). That joins another successful model, the ET5, which is available in don’t call it Touring a station wagon version. This station wagon version contributes to roughly a third of all ET5 sales, an amazing result in an otherwise station wagon averse market. But then again, just look at it — not only is it the most attractive NIO model right now, but it’s also one of the most beautiful station wagons around. Kudos, NIO!

Still on the startup field, Hozon’s Neta Aya has landed with 5,609 units. The Aya is basically a refreshed Neta V, so it will be interesting to see where it finds its cruising speed. Will it get to 10,000 units/month?

Looking at Changan’s new Premium brand, Deepal, the new S7 midsize SUV reached a record 8,891 registrations, so we might have another Model Y fighter joining the table soon.

Finally, from foreign OEMs, the highlights are the VW ID.3’s 7,485 registrations, confirming that price cuts can do miracles to one’s career, and the BMW i3. That’s not the future classic quirky hatchback, but in this case, the China-only BEV version of the BMW 3 Series. After a slow start (due to an inflated price), it is now selling okay (5,290 registrations) thanks to a recent price cut.

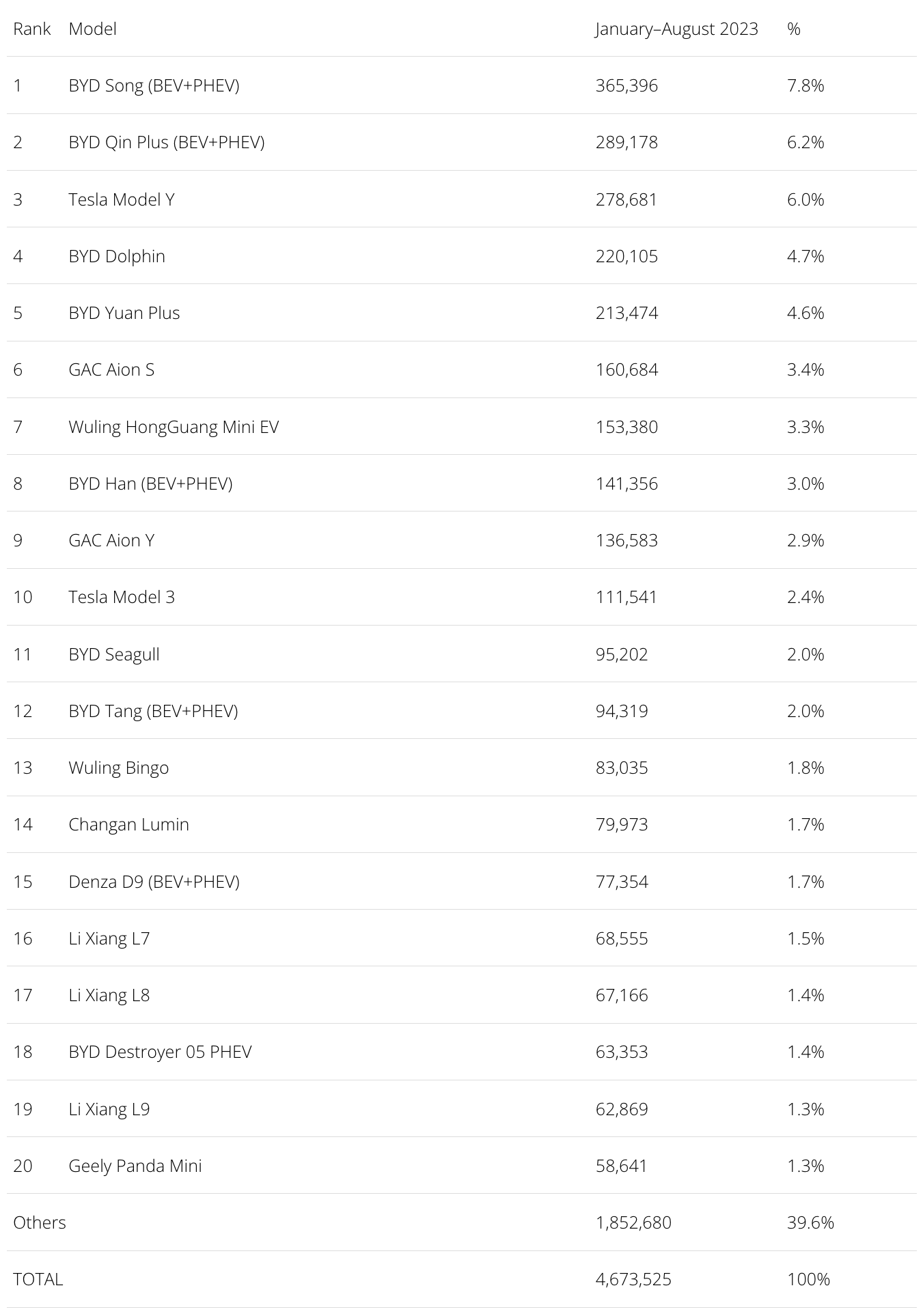

The 20 Best Selling Electric Vehicles in China — January–August 2023

Looking at the 2023 ranking, the BYD Song is well above the competition, while the runner-up BYD Qin Plus has kept the #3 Tesla Model Y at bay. Will the Chinese sedan resist the US crossover’s pressure in September?

Off the podium, the BYD Dolphin is the new 4th placed model, switching places with the BYD Yuan Plus. The BYD Seagull continued its unstoppable rise, jumping four positions in August to #11. Expect it to jump a few more positions by the end of the year.

Still in the second half of the table, we have another BYD on the rise, with the Destroyer 05 climbing one position to #18. It switched places with the pachydermal Li Xiang L9.

Despite this setback, we must mention that all three Li Auto models are in the top 20. Apart from the all-mighty BYD, no one else has that many models in the top 20, and it helps to explain why this is the hottest EV startup right now. In four years, Li Auto went from 0 to 500,000 units delivered!

Top Selling Auto Brands & Auto Groups in Chinese EV Market

Looking at the auto brand ranking, there’s no major news. BYD (35.2%, down 0.3%) remains stable in its leadership position and is looking to win its 10th plugin automaker title this year, while off-peak Tesla (8.4%) is stable in second place.

Third-placed GAC Aion continued its slow but steady rise, going up to 6.6%, a slight increase from its 6.5% in July. Meanwhile, the SGMW joint venture’s performance was back in red, dropping its share from 5.9% in July to its current 5.6%.

Finally, 5th placed Li Auto continues on the rise (4.5%, up from 4.4%). The startup is going from strength to strength, reaching consecutive record sales and looking set to become a force to be reckoned with in the future.

Despite staying off the radar of many analysts, Li Auto’s growth potential, price points, and margins are the most promising among current EV startups. Just to put the company’s amazing growth curve into context, in 2015, three years after the Model S launch, Tesla was celebrating a record 50,000 sales a year. Li Auto hopes to do that in December alone….

This is kind of a perfect s*** storm for legacy OEMs in China, with BYD and GAC going after their mainstream market volumes, Tesla hitting their midsize/premium offers hard, and Li Auto eating its way into the last bastion of profitability for foreign OEMs in China: full size models.

Looking at OEMs/automotive groups/alliances, BYD is comfortably leading with 36.9% share of the market, down 0.4% in August, while #2 Tesla (8.4%) remains stable. The SAIC mothership was in the red, and the SGMW JV did not have a good month. The Shanghai-based OEM was down from the 7.5% share it held in July to its current 7.2%, which was enough still to allow it to retain the last position on the podium.

But, with rising #4 GAC (7.1%, up from 6.9%) dangerously close, SAIC could have its bronze medal in danger in September.

One step down, #5 Geely–Volvo is slowly growing, now at 5.8% share, up 0.2% share compared to the previous month.

With #6 Changan still at 4.5%, Li Auto (also at 4.5%) is looking to surpass it in September, so next month could bring two position changes in the OEM race.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Video

CleanTechnica uses affiliate links. See our policy here.