Putting China’s Coal Consumption in Context

The United States and China are going in the opposite direction on coal.

I’m a little surprised by the optimism in this week’s “World Energy Outlook 2022” from the International Energy Agency. For the first time, the IEA is predicting that “coal demand peaks within the next few years”. David Wallace-Wells in this weekend’s New York Times Magazine has a similarly optimistic view, arguing that the worst climate outcomes are now much less likely, largely because the world is shifting away from coal.

I’d like to believe this. But, I am having trouble reconciling this optimism with recent data on coal consumption. Total global coal consumption increased 5% in 2021, and global electricity generation from coal last year reached an all-time high.

This continued reliance on coal reflects, in part, a multi-decade coal plant building binge in China. Last year over half of all coal-fired electricity generation came from China, so understanding the country’s trajectory for coal consumption is critical for global efforts to address climate change.

For today’s post, I want to look at data on electricity generation from coal in China. How much electricity does China generate from coal? How has this changed over time? And, to put this into context, I want to compare this to the United States, where the industry is going in a sharply different direction.

Trading Places

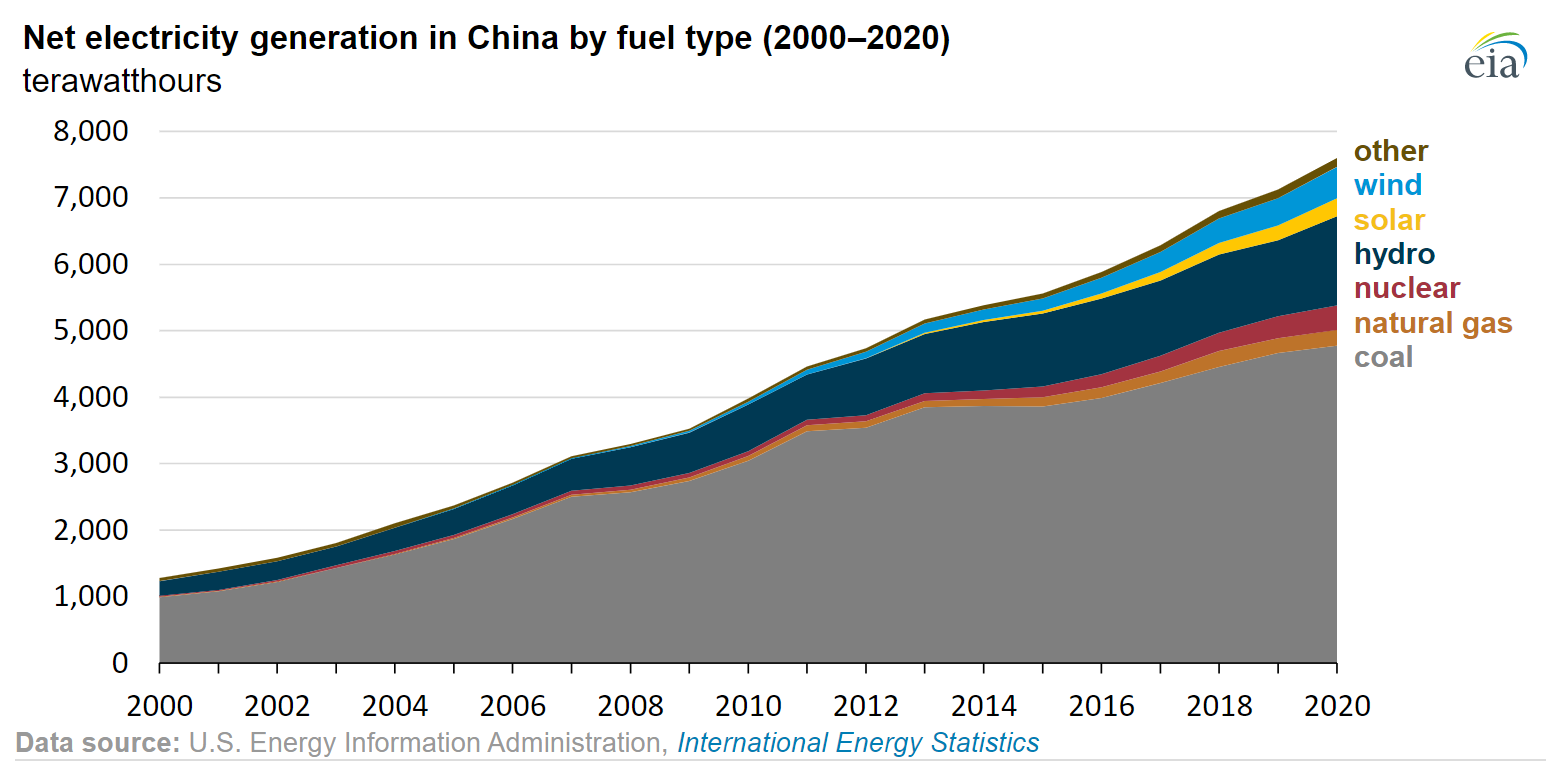

The figure below plots annual electricity generation from coal. Other sectors use coal too, but electricity generation is the most important.

–

In 2000, the United States generated 2,000 TWhs of electricity from coal. This was peak U.S. coal consumption, with just under one billion tons of coal burned for electricity generation, the equivalent of 3.5 tons of coal per person.

Since that time, U.S. electricity generation from coal has declined steadily, reaching 770 TWhs in 2020. This is still a lot of coal, but the overall pattern since 2000 is a remarkable decline that has been widely studied (here, here, and here).

China Powers Up

China has been going in the opposite direction. From below 1,000 TWhs in 2000, electricity generation from coal in China reached 4,775 TWhs in 2020. I’m struck both by the rapid growth in China, and by the wildly divergent patterns for the two countries. China goes from 0.5x the United States, to 6x the United States by 2020.

The biggest single factor explaining the divergent patterns is that China’s demand for electricity is soaring, while U.S. demand is practically flat.

–

To meet this massive increase in demand for electricity, China has built more of everything. More wind, solar, hydro, and nuclear than any other country, and yes, much more coal.

This continued dominance of coal has many implications. For example, it makes me think about the environmental impact of electric vehicles. From a climate change perspective, electric vehicles in the United States make more sense than they did even just a few years ago. But the case is harder to make in China with a coal-dominated grid, even as the country leads the world in new electric vehicle sales.

What’s Next for China?

It is always hard to predict the future. Nicholas Stern and coauthors predicted in 2016 that China’s coal use had already peaked, and that economic growth in China had been “decoupled” from growth in coal. Now with the benefit of a few more years of data, those predictions seem pretty clearly wrong.

If anything, coal in China seems to be gathering momentum. While coal recedes in other parts of the world, China is adding dozens of gigawatts of coal generating capacity each year, the equivalent of one new large coal plant per week. And a recent report finds that China has 247 gigawatts of new coal power plants under development.

On the other hand, a recent study by Energy Institute alum Amol Phadke and coauthors finds large opportunities for China to substitute away from coal. In their analysis, large-scale investments in solar, wind, and battery storage create a Chinese power sector that is both lower-cost and much lower-emitting.

Big Ship

I’m not sure what is going to happen, but I do know that much is at stake. One of the authors of a recent related study spoke about the inherent inertia in electricity markets, “China is like a big ship, and it takes time to turn in another direction.”

One important element of this inertia is coal plants themselves. Coal plants have a typical operating lifespan of 35 years or more, so every time a new coal plant is built, this threatens to lock in decades of future carbon dioxide emissions.

It is a reminder, as well, to take any predictions with a large grain of salt. Yes, there are reasons for optimism, and opportunities for decarbonization that simply did not exist a few years ago. But coal and other fossil fuels are still cheap, convenient, and used in vast quantities around the world.

–

Keep up with Energy Institute blogs, research, and events on Twitter @energyathaas.

Suggested citation: Davis, Lucas. “Putting China’s Coal Consumption in Context,” Energy Institute Blog, UC Berkeley, October 31, 2022, https://energyathaas.wordpress.com/2022/10/31/putting-chinas-coal-consumption-in-context/

Categories

Lucas Davis View All

Lucas Davis is the Jeffrey A. Jacobs Distinguished Professor in Business and Technology at the Haas School of Business at the University of California, Berkeley. He is a Faculty Affiliate at the Energy Institute at Haas, a coeditor at the American Economic Journal: Economic Policy, and a Research Associate at the National Bureau of Economic Research. He received a BA from Amherst College and a PhD in Economics from the University of Wisconsin. His research focuses on energy and environmental markets, and in particular, on electricity and natural gas regulation, pricing in competitive and non-competitive markets, and the economic and business impacts of environmental policy.

Very useful article, especially the graph charting electricity generation. When will 2021 data be available?

The usage of coal and other fossil fuels is determined by the energy demands of industry and homes for electrical power. I cannot change what industry does, but I can change what this homeowner and other homeowners around the world can do by encouraging rooftop solar panels with battery storage. This is a “can do” way of reducing greenhouse gases. By installing enough solar panels, twice or even 3 times what is recommended, or even allowed by utilities, is the only way to get the fossil fuels power plants into decline. When the summer demand drops off, so will the fossil fuel plant building frenzy be forced to stop due to “economic concerns” that the new plant won’t be able to pay for itself.

The electrical infrastructure around the fossil fuel plants can later be used for solar panels, batteries and even wind farms like at Moss Landing in Monterey, California has done. I no longer use fossil fuel Natural Gas in my home thanks to my very large NEM summer bank of extra electricity I send to the grid. The PG&E mix of only 8% fossil fuels electrical power means I am not using just fossil fuels to heat my home with electricity but a mix of Nuclear, Solar, Wind, Bio, Geothermal and Natural Gass instead of 100% Natural Gas. it will take time for the rest of the world to catch up to what i have done but the enthusiasm I see for rooftop solar is very encouraging.

‘Lower’ cost than coal for the Chinese , based on batteries and intermittants, is a baseless claim with more ‘magical thinking’ than economist thinking. China will continue ramp fossil fuels and CO2 output on an absolute basis for many decades to come. As pointed out, coal plants have a useful life of 35-40yrs+. Building 1 new coal fired plant per week in China shows the reality over Eco diplo-speak and hope as a pla.

Thank you, Lucas, for the interesting and thoughtful article.

There are a couple of “adds” which are worth considering—-but certainly don’t bring sunshine.

Much (most?) most of the coal electricity plant retirement in the U.S. has been offset by new or converted natural gas plants. Yes, natural gas burns cleaner and less carbon intensively than coal, but is in no way a long term solution for carbon mitigation.

China provides substantial subsidies to its electricity generation industry—-including coal and solar. Coal subsidies continue without pause; however, past due payables for Chinese solar PV provided to the grid have continued to grow with Bloomberg estimating some $60B + outstanding. The entire U.S. electricity industry’s annual revenue is slightly north of $400 B.

No easy answers here, and to some degree nothing new under the sun.

Good article. The takeaway is that our current U.S. and European carbon reduction strategies are counterproductive and destined for failure. Until we choose policies that “reach out” to influence China, India, and other rapidly growing economies to decarbonize, we are only weakening our own economies (by exporting CO2 emitting industries) and reducing pathways to the middle class in our societies. We shall see if voters believe our existing U.S. policies are effective and fair on Nov. 8th.

The choices in this year’s election are between having a climate change policy vs. denial that climate change matters and full steam ahead on fossil use. There’s no “middle way” being offered by the latter party.

Richard, a pleasure to agree with you here – although the “energy transition”, mostly due to supply constraints, is itself in a stage of transition.

“The biggest single factor explaining the divergent patterns is that China’s demand for electricity is soaring, while U.S. demand is practically flat.”

China’s population has been leveling off since ~2018, and in 2021-2022 the country experienced zero percent population growth for the first time in recorded history. Demand for electricity is soaring, due both to improvements in the Chinese economy and living standards – but per capita, Chinese CO2e emissions are still half of those of the U.S. We can expect continued growth in consumption and emissions, at least until parity is achieved.

IMO in the long view (isn’t any view that considers climate change a long one?) coal is demonized unfairly in comparison to natural gas. With the recent finding that up to 3% of natural gas escapes in the form of “fugitive” emissions, there is the distinct possiblity gas is a greater contributor to climate change than coal, on a per-unit-of-energy basis.

Though I’ve used the word “possibility”, a better one would be “likelihood.” Although natural gas (methane) decomposes to carbon monoxide/dioxide relatively quickly, it’s anywhere from 28% to 80% more effective at capturing the radiant energy in sunlight than CO2. In one analysis that assumed only 2% fugitive emissions, gas was 2.4 times worse for global warming than coal. Though a lot depends on other assumptions, the sooner all fossil fuel combustion is minimized, the sooner we can begin to make real progress with climate change. And no matter how soon that is, it can’t be soon enough.

An excellent article with important implications concerning global GHG emission trends, how emissions are partitioned by country, and how realistic or not goals like 1.5 degrees are given the trends in emissions by China (and India). Kudos to Prof. Davis for considering externalities outside the borders of California.

I’d also like to put in a plug for the excellent working paper by Rapson and Bushnell on The Electric Ceiling: Limits and Costs of Full Electrification. This paper should be required reading by all energy policy makers in California and the Nation.

Nice to see the Energy Institute putting out these impactful studies.

I agree with Lucas’ skepticism. In a sense the newest IEA forecasts seem to consciously ignore the sizeable investment and direct technological contribution of Chinese coal technology to states in Africa. Early regulatory and planning estimates of lifespan for coal plants in the US was an optimistic 45 years. The likely capability of these plants (ignoring for a second technology emissions standards) is even greater, perhaps double that number, locking in the demand for this specific fuel and ensuring the emissions characteristics Lucas cites. Consequently, the built-in demand for coal as a fuel could actually extend through this century. We may “decommission” coal facilities, but as a practical matter they tend to remain in place and don’t get dismantled; a kind of silent malignant reserve on the landscape for very long periods of time. Lets face it, future regime changes could reverse current regulatory preferences and bring them back to life.