What Does The IEA 2023 Renewables Update Tell Us We Should Pay Attention To?

For years, the International Energy Agency would provide updates on the historical growth of renewables globally, and then project them in a flat line into the future, often with slowing growth after a few years. And every year since 2002 and at least through 2020, their forecasts were laughably, radically wrong. Auke Hoestra, program director of the NEON research initiative at Eindhoven, had annual fun publishing how absurdly wrong they were.

Why this was is easy to understand. The IEA is a global organization that for the vast majority of its history was about oil, gas, and coal. Electrical generation that it was concerned with was centralized, and mostly consisted of custom engineered, very large, singular units. The growth of those forms of energy was rapid, but not exponential. Its analysts — while not stupid, and having access to lots of data — were stuck in a paradigm that didn’t understand modularity, manufacturability, global supply chain advantages for manufactured goods, and parallelization of construction. As a result, every year they did a simple induction based on the previous year’s curves. And every year they were proven wrong, as the actual growth function was exponential. We all have our biases that are hard to overcome.

I stopped paying attention to their forecasts almost a decade ago. However, their 2023 forecast crossed my screen and there a few insights in there.

First off, their forecasts for renewables aren’t terribly wrong any more. They are projecting growth of 107 gigawatts of new capacity over installations in 2022, for a total of 440 GW in new capacity this year. 32% growth year over year is indicative that they’ve finally realized growth rates aren’t linear. I suspect that their main case is going to be proven wrong, as China built 47.4 GW of wind and solar in the first quarter alone. However, they have an accelerated case of 500 GW of new capacity. I suspect that’s more likely to be accurate, and as a note, that represents a 50% year over year increase. Clearly, the IEA analysts finally got the memo that they were embarrassing themselves.

As always, western analysts tend to overstate the global challenges facing the wind energy sector. Western manufacturers are facing supply chain issues, which is unsurprising given the significant trade hostility shown toward China, which is the primary minerals processor and component manufacturer for key aspects of wind turbines. Western wind turbines are getting more expensive, and western NIMBYs continue to hinder onshore wind energy. Meanwhile, those supply chain problems are inverted for Chinese manufacturers like Goldwind, Envision, and Minyang, which are churning out high-quality onshore and offshore wind turbines for domestic and international markets willing to buy them.

Chinese firms are now six of the top ten turbine manufacturers on the planet, and Goldwind isn’t lagging Vestas or Siemens Gamesa by much. Chinese firms are producing about 46% of wind turbines installed globally. Meanwhile, GE sank to fourth in 2022. While there’s a good deal of chauvinism from the west, it’s possible to get equally high-quality turbines at a significantly lower price from China than from western firms today.

As I said in my ESG Frontier Dialogue seminar with Beijing’s Tsinghua PBC School of Finance recently when asked about the implications of the EU’s carbon border adjustment mechanism, the combination of China’s purchasing power parity and Wright’s Law advantages meant that Chinese firms should be able to undercut western manufacturers and still make a good profit. The only thing that would stop western firms buying equal quality but cheaper Chinese products was full on protectionist banning of them, and that would occur on only a narrow slice of products.

Just as China’s electric cars are now displacing European cars on its roads, just as Chinese solar panels are everywhere in the world, China’s wind turbines will increasingly be the product of choice globally. The IEA is a little light on that reality, merely noting that “Western wind manufacturers face challenges from high commodity prices.”

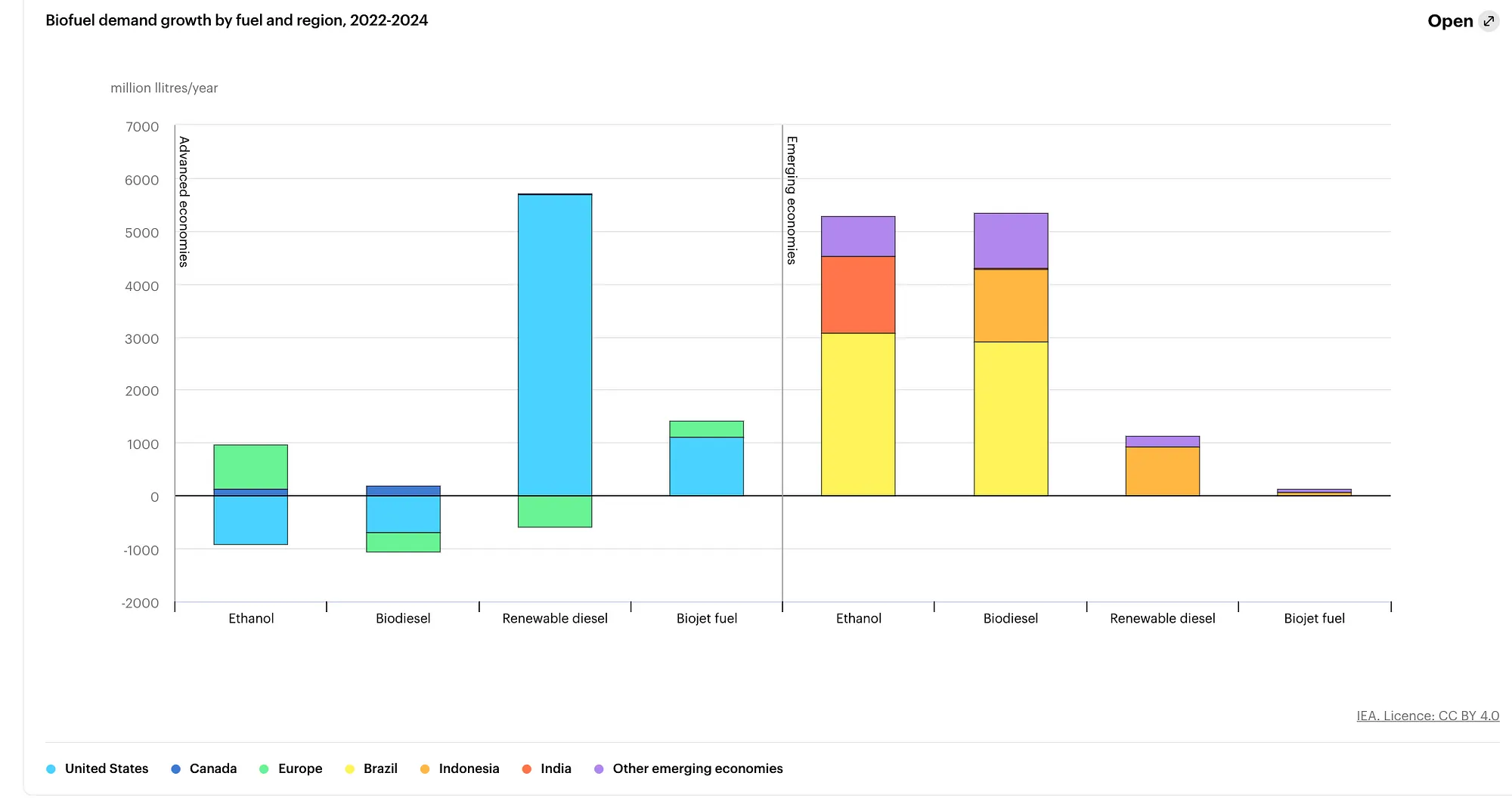

The big story for me out of the forecast, however, was biofuels.

As a green infrastructure fund executive I was talking with around an engagement to assist them with their next multi-billion-euro fund said, they’ve been hearing for years that synthetic green fuels would be taking over the market any day now. And every year, the story is the same, with no synthetic green fuels outside of very limited run examples.

Meanwhile, biofuels.

Let’s step through these. Ethanol is made currently from corn and sugarcane, using 8,000-year-old fermentation and 6,000-year-old distillation technologies. Biodiesel is made from vegetable oils, animal fats, or recycled restaurant grease. Renewable diesel is made by upgrading ethanol and other biological pathway materials through pyrolysis, hydrotreating, gasification and a couple of other technologies. (That it’s called “renewable diesel” probably confuses people who think it means synthetic diesel manufactured from hydrogen, carbon, and oxygen atoms using renewable electricity, but that isn’t what it is.) Biojet fuel is a biokerosene made in the same ways that biodiesels and renewable diesels are.

There are a bunch of biofuel pathways represented there, and for people interested in the vast array of feedstocks available, I recently put together a reasonable survey of the big ones.

Sharp eyes will note something missing from this chart and data: China. That country doesn’t typically provide transparent data to the rest of the world, but on everything that it does share, it’s vastly ahead of everybody else. EVs? 60% of total world market. High-speed freight and passenger rail? Heading for 70% of the world’s deployed rail. Steel? Manufacturing as much as the rest of the world combined and ten times as much as 2nd place India. Etc, etc, etc.

Assuming that China’s biofuel manufacturing is at least within the same order of magnitude as the rest of the world is a safe bet, and it’s missing from this data as far as I can tell. (If an IEA boffin reading this knows better, please let me know.)

The chart adds up to just under 20 billion liters of biofuels growth. Sharp eyes again will note that while ethanol tends to get the attention, biodiesel, renewable diesel, and biojet fuels consist of vastly more of the market. They are, after all, plug compatible with existing jet and maritime engines, and can be mixed with existing fossil fuels for those segments without new tanks or ships.

20 billion liters is an interesting number. A liter is about a kilogram, so that’s about 20 billion kilograms, or 20 million tons of fuel. That doesn’t sound like a lot, but remember that it’s demand growth year over year, not actual production. The IEA forecast asserts that biofuels avoided about 2 million barrels of oil equivalent per day in 2022, or about 4% of global transport sector oil demand. 2 million barrels of oil a day for a year is about 100 million tons, although the units are very imperfect in this coarse calculation.

20 millions tons is a big expansion of demand, 20%. The chart does represent 2022-2024, so let’s assume that’s 10% per year. Still respectable. It might be 2022, 2023 and 2024, or three years, which would be just under 7%, which is still pretty good. Is this likely to be correct? I don’t think so.

Finnish biofuels giant Neste just announced its Singapore biofuels plant next to Changi Airport has expanded from 1.3 million tons annually to 2.6 million tons. About a million tons of that is expected to be sustainable aviation fuels (SAF), aka the biojet fuel the IEA has in this data. A single plant in Singapore just turned on 7% of the capacity of the IEA’s projected demand increase for biofuels for two to three years.

I spend a lot of time looking at transportation repowering alternatives. I’ve done assessments of all options and projected scenarios for ground transportation (so close to 100% electrification that the remainder is irrelevant), aviation (increasingly electrified through 2100, with SAF biofuels bridging in diminishingly hybrid models), and maritime shipping (all inland and ⅔ of short sea shipping battery diminishingly hybrid electric, the remainder in biodiesel).

Methanol and ammonia are touted as new maritime fuels. What’s the status? Well, Maersk has contracted for bio-methanol, that is methanol manufactured from biologically sourced methane instead of fossil methane, with 50,000 tons expected in 2024. As I noted recently, I’m leery of any energy pathway that goes through anthropogenically created biomethane, as intentionally manufacturing more high global warming potential gases seems like a bad idea to me. But at least it’s not synthetic methanol, which would be even more expensive. Biomethanol is likely 2–3 times the cost per ton of fossil methanol, which means that on a unit of energy basis, given it’s 45% energy density, it will be 3–4 times the cost of current diesel. I don’t see that penciling out in the long run. And if it does turn out to be the maritime fuel of choice despite its drawbacks, it will still be a biofuel, not a synthetic fuel.

No green ammonia shipping fuel contracts have been signed as far as I can tell. Given the challenges with price, energy density, capex for dual fuel ships and bunkering of those fuels, it’s unclear to me why the maritime industry isn’t leaning into biodiesel. That’s starting now, it seems, per discussions with Stena representatives in Glasgow recently, when they flew me there to participate in a maritime repowering debate. To be clear, there’s no real biomass feedstock pathway to ammonia as there is with methanol, so it will be even more expensive.

What I see in the IEA alternative fuels material are three things.

The first is that they are probably as wrong about biofuels as they used to be about renewables. They are having trouble seeing reality due to their cognitive biases. Someone will probably be doing what Auke Hoekstra was doing for years with mocking reprisals of their failures. It’s unlikely to be me, so someone with an appetite for annual mockery, please self select.

The second is that my projection of biological pathways to maritime diesel and aviation kerosene are exactly what’s happening in the real world of the hydrogen hype bubble eating up Europe, North America, Japan, and Australia right now.

And the third is that 4% of all transportation fuels globally is not that far off what will be required once all ground transportation and more aviation and maritime shipping electrifies. We don’t need to make 25 times as much biofuel, we need to make perhaps four or five times as much as we do today. And we have to stop wasting it on ground transportation.

Mea culpa: an earlier version of this article got the tonnage of biofuels additional demand wrong. Thank you to the sharp-eyed reader who pointed out my mistake.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Video

CleanTechnica uses affiliate links. See our policy here.