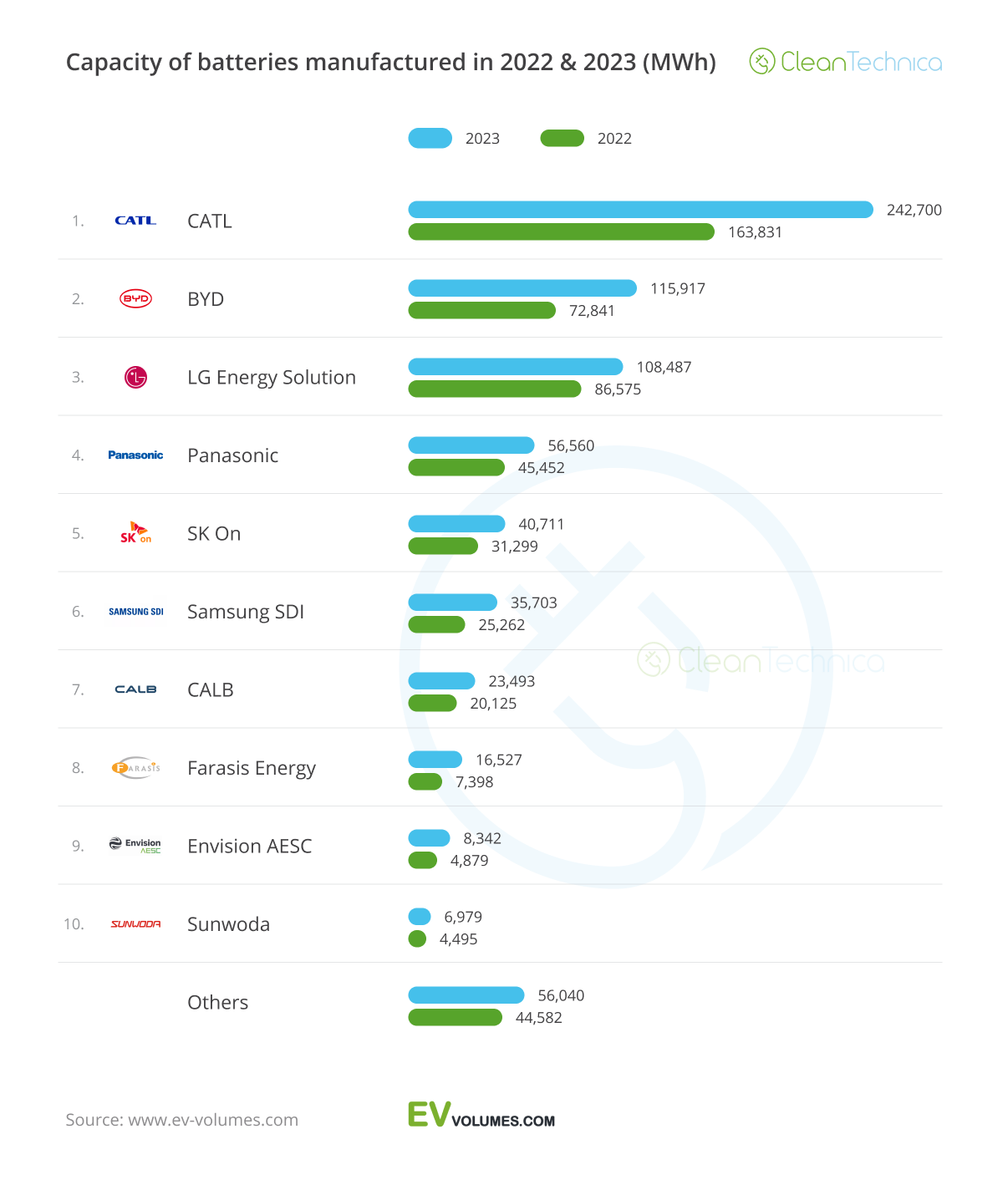

Top 10 Battery Producers In The World — 2023 (Provisional Data)

While there are regular reports about sales performances of the best selling EVs, as one can see here, here, and here, reports on the deployment of the all-essential batteries for these EVs are much less frequent. Nevertheless, they are a critical element in the EV transition, and big business too.

In this provisional report on 2023, demand for lithium-ion batteries in the light vehicle automotive sector grew around 40% last year, up to 712 GWh from 507 GWh in 2022. So, which companies are leading the way in supplying the EV industry?

Taking Charge at the Top

Batteries for light electric vehicles (cars, SUVs, LCVs, and pickup trucks) had a faster production growth rate (+40%) than EVs (+35%) in 2023, as the market had several models introduced with bigger batteries, while others had their batteries super-sized.

CATL continues to lead the charge, and it has increased its share from 32% to 34% due to a slightly over-average growth rate. That’s thanks to the continued success of the Made-in-China Tesla Model Y, SAIC’s MG4/Mulan, Li Auto’s success, as well as a looong list of clients. With the recently introduced Qilin battery and promising new Shenxing batteries, expect the battery maker to consolidate its share and remain in the lead through 2024, and even for years after that.

Fast growing BYD (+59% YoY) is the new silver medalist, with the Chinese everything battery maker jumping from 14% in 2022 to 16% in the same period of 2023 thanks to the rise and rise of the namesake brand. But the growth is also due to the new 3rd party supply deals it now has. It supplies the Made-in-Germany Tesla Model Y, Toyota bZ3, Changan UNI-V, Venucia V-Online, as well several Haval and FAW models. And with other brands lining up to get their batteries in 2024 (Kia, KG Mobility, etc.), expect the Shenzhen make to continue increasing its share throughout the year.

This was done at the cost of LG, which lost share in 2023, going from 17% in 2022 to 15% by the end of 2023. This was due to the lack of new orders, GM’s troubled ramp-up of its new EVs, the end of life of some important volume models (Renault Zoe…), and also the fact that volume from some clients, like Mercedes or Ford, is being diverted to the competition.

Still, the top three battery makers are responsible for two thirds (66%) of the total battery deployment, which highlights the importance of scale in this business, in order to have the most competitive product on the market.

Panasonic, once upon a time a leader in the automotive EV business, has continued its slow slide down the table. It’s now in 4th, with 8% share, down from 9% last year. With its main client, Tesla, now effectively a multi-supplier OEM when it comes to batteries, and without another large client coming to fill in the gap, the Japanese battery maker is losing in this race. This is also in no small part due to the small EV investments that its compatriot automotive companies are pursuing.

#6 Samsung SDI followed the market, helped by increasing volumes at Jeep and the production ramp-up of Rivian, while slow growing CALB was in 7th. But the highlights are coming up behind. First of all, #8 Farasis Energy (+123%!) is the biggest highlight, having seen its share grow from 1% in 2022 to its current 2%. The Chinese company is now looking to displace CALB from the 7th spot during 2024. That’s thanks to the success of GAC, the addition of Mercedes as a large client, and the ramp-up of the nascent Turkish startup Togg.

#9 Envision AESC (+77%) and #10 Sunwoda (+55%) are also growing above average. They’ve seen significant growth rates. For AESC, the ongoing relationship with Nissan is the bread and butter of the company, but the big reinforcement this year is the addition of the US operations of Mercedes. While it is not significant in the total number of EVs sold, when we remember that each EQS SUV has a 108 kWh battery … it does make a difference. Finally, Sunwoda is greatly benefitting from the growth of the startup Leap Motor, which it is the main battery supplier for.

With the EV market continuing to grow fast, and average battery size increasing, expect the battery market to continue growing even faster, with +/-50% growth rates likely in the next couple of years.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Video

CleanTechnica uses affiliate links. See our policy here.